As the cannabis industry expands, so does the complexity of its risk. One of the emerging issues is cannabis motor truck cargo, which involves unique exposures and liabilities. One of the most alarming trends we continue to uncover at Spire Insurance Solutions is this:

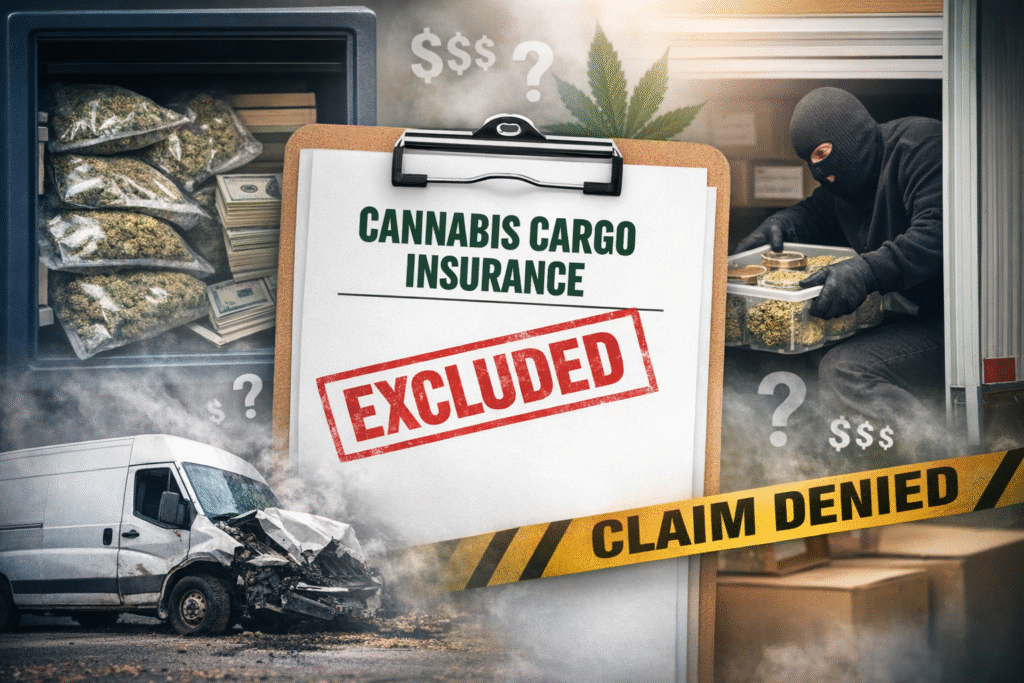

Most cannabis transporters — and even many dispensaries, cultivators, and manufacturers — are carrying cargo insurance that DOES NOT cover cannabis.

That’s right.

Even though businesses believe they’re insured for product in transit, the policy language often tells a very different story.

In this blog, we’ll break down:

- Why this coverage gap exists

- Where the exclusion is hiding

- Why your insurer may not have caught it

- How to fix it before a claim is denied

- What every cannabis business should be reviewing right now

The #1 Issue: Cargo Policies That Exclude “Marijuana Products”

Across dozens of recent policy reviews, we found the same pattern:

Standard Motor Truck Cargo policies frequently include buried exclusions listing “marijuana products” — even when the insured is a licensed cannabis operator.

These exclusions often group cannabis in with:

- Pharmaceuticals

- Tobacco

- Alcohol

- Controlled substances

- Contraband

A business may be paying thousands annually for cargo coverage…

…but if cannabis is excluded, that premium does nothing for you when the load contains THC products.

This means:

❌ A theft = no coverage

❌ A crash = no coverage

❌ Lost or damaged product = no coverage

❌ Temperature spoilage = no coverage

One claim can wipe out a transporter or destabilize a vertically integrated operator.

Why Cannabis Operators Are Missing This (It’s Not Their Fault)

1. Declarations pages don’t show exclusions.

Most companies only see the front page — the “dec page.”

But exclusions live 4–10 pages deeper in the policy forms.

2. Many generalist insurance agents don’t specialize in cannabis.

They may not know to check for “marijuana product exclusions,” “Schedule I language,” or “contraband clauses.”

3. Standard carriers still consider cannabis federally illegal.

Even in legalized states, carriers often use federal status as justification to exclude THC-containing products.

Where the Exclusion Hides (Look for These Red Flags)

When reviewing your policy forms, search for these keywords:

🚫 “Marijuana Products”

🚫 “Cannabis” or “THC-containing products”

🚫 “Contraband”

🚫 “Illicit trade or transportation”

🚫 “Schedule I substances”

If you see those words in your cargo forms, you likely do NOT have cannabis cargo coverage.

The Financial Risk Is Much Larger Than Operators Realize

Most cannabis transporters routinely carry:

- $50,000–$150,000+ of flower

- $80,000+ of vapes or concentrates

- $20,000–$60,000 of infused products

- Sometimes cash as well

One theft or vehicle loss = catastrophic out-of-pocket exposure.

Many operators assume “that’s what insurance is for” — but if cannabis is excluded, the insurer will not pay.

We’ve seen claims denied for:

- Smash‑and‑grabs

- Rollovers

- Temperature swings

- Driver error

- Warehouse staging issues

- Mixed manifest errors

Once the insurer points to the exclusion, the case is closed.

How to Fix the Cargo Coverage Gap Immediately

✔ 1. Review the actual forms — not the declarations page.

We can do this for you in minutes.

✔ 2. Pair standard Auto Liability with a cannabis‑approved cargo policy.

This is often the best cost‑control strategy.

✔ 3. Move cargo coverage to a cannabis-specific carrier:

Some of the insurers include:

These carriers explicitly insure cannabis and THC products.

✔ 4. Re-check your contracts and terms of service

If you state you carry cargo coverage — but the carrier excludes cannabis — you may be unknowingly out of compliance.

The Bottom Line

If you are transporting cannabis — or hiring a transporter — you absolutely must confirm whether your cargo policy actually covers THC products.

At Spire Insurance Solutions, we have uncovered this same exclusion again and again, even for companies that were explicitly told their cargo was covered.

We’re here to change that.

Cargo Policy Review (No Pressure. No Sales Pitch.)

If you want us to review your cargo forms to confirm whether you’re actually covered, just reach out.

👉 Schedule a call today to talk about your cannabis-specific insurance solutions.

Spire Insurance: Your Partner in Cannabis Business Protection

At Spire Insurance, we have been helping cannabis companies throughout the country from Michigan to Colorado, in Minnesota to Maine, or Arizona to Missouri. Whether it’s cannabis and hemp insurance, our conversations can help ensure you receive the necessary coverage without overpaying, allowing you to focus on growing your business confidently.

Estimate the Cost of Your Cannabis Insurance

Don’t let high premiums hold your business back. Get started with our Cannabis Insurance Calculator to estimate insurance needs for both your cannabis and hemp ventures.

We’ve shared some helpful resources including information on buying cannabis insurance:

- Cannabis Business Insurance Cost Breakdown and Factors

- Vetting Cannabis Insurance Agents: The Ultimate Checklist

- Finding the Right Insurance Agent for Your Cannabis Business

- The Reality of Cannabis Business Insurance: Why Multiple Agents Aren’t the Answer

- Key Factors to Consider When Choosing Cannabis Insurance